Why the private energy buildout is creating a supplier opportunity that everyone else is missing.

This is the first in a three-part Trend Watch series on what’s actually changing in energy, beyond the daily headlines about policy fights and AI demand. The argument across these three pieces: the energy economy is being rebuilt from the ground up. I believe the supplier opportunity is bigger than anyone is talking about.

What Changed?

In September 2024, Microsoft signed a 20-year power purchase agreement with Constellation Energy to restart Unit 1 of Three Mile Island. Yes, that Three Mile Island. The plant had been shut down since 2019, mothballed after it couldn’t compete with cheaper natural gas. Now, Constellation will spend $1.6 billion to bring it back online, targeting 2028. The facility has been renamed the Crane Clean Energy Center. Every megawatt it generates, all 835 of them, will go to one company – Microsoft.

This is not how the energy business is supposed to work.

For roughly a century, the model was simple. Utilities built power plants. Customers, including very large ones, bought electricity from those utilities at regulated rates. Even the biggest industrial users were, fundamentally, retail buyers. They negotiated terms. They didn’t commission their own reactors.

But that model is breaking. In any other timeline, the Microsoft deal would be considered an outlier. It’s quietly becoming the new template.

In 2025, Amazon Web Services signed a 17-year agreement with Talen Energy to take 1.92 gigawatts directly from the Susquehanna nuclear plant in Pennsylvania. Google signed a fleet agreement with Kairos Power to deploy small modular reactors by 2030, alongside separate geothermal deals with Fervo Energy. Amazon has invested $500 million in small modular reactor development of its own. Meta signed a 20-year deal with Constellation for the entire output of the Clinton Clean Energy Center in Illinois — 1.1 gigawatts beginning in June 2027. And Meta has also disclosed an even larger 6.6 gigawatt nuclear procurement strategy to support its “Prometheus” AI data center project. For context, that’s more electricity than the peak demand of the city of Chicago. Going to one company. For one project.

Stack those announcements together and you can see the pattern. The largest power consumers in the country are no longer waiting for utilities to build what they need. They’re commissioning their own infrastructure, signing private agreements with generators, and in some cases buying entire plants. They’re exiting the consumer side of the utility model and building their own energy fiefdoms instead.

That shift is the single most important thing happening in American energy right now. And almost no one is framing it that way.

Why Does It Matter?

Most of the mainstream energy conversation is, understandably, still focused on supply and demand. How much power will the grid need? Where will it come from? Can renewables scale fast enough? Will gas plants get permitted? Those questions matter. They’re also a generation behind the actual story.

The actual story is more profound, with much bigger implications for all of us. So, what happens when the biggest customers stop relying on the utility companies? Three things.

First, the financing model changes. A traditional utility raises capital based on regulated returns and recovers costs through rate base over decades. A hyperscaler buying a nuclear plant is doing a different kind of math. They have the balance sheet to underwrite the entire project against their own consumption. That makes some projects pencil out that wouldn’t have otherwise. It also concentrates risk in a way the system hasn’t ever had to plan for.

Second, the procurement model changes. When Microsoft signs a 20-year power purchase agreement, they’re not just buying electrons. They’re buying all the infrastructure and any new capacity. They also have a direct stake in site selection, permitting timelines, construction quality, fuel logistics, cybersecurity, and the ongoing operations. Decisions that used to live inside a regulated utility, that were invisible to most, now live inside a procurement function at a tech company. This is the upside, the potential payout, for companies nimble enough and in-the-know. Those procurement teams are sourcing differently, and they’re sourcing fast.

Third, the supplier model changes. This is the part that matters most for OMSDC’s community. And it’s the part the trade press has barely started to cover. A century-old utility has an established supplier bench. They’ve worked with the same engineering firms, the same EPC contractors, the same equipment vendors, for decades. It’s difficult for someone new to get a toe in the door. But when a tech company decides to build its own energy infrastructure, that bench doesn’t transfer automatically. The supplier ecosystem has to be rebuilt for a new kind of customer, with new requirements, on a new (faster) timeline.

That’s the opening. That’s your foot in the door.

The Supplier Ecosystem Most People Haven’t Mapped

When a hyperscaler commits to a multi-billion-dollar energy project, they need more than a generator. They’re doing an entire buildout. Each layer of that buildout is a supplier opportunity, and most of them are categories where our minority-owned businesses already have real capability.

Site selection and acquisition. Permitting and regulatory work. Civil and structural construction. Heavy electrical contracting at industrial scale. Mechanical, HVAC, and cooling systems. Controls and automation. Fuel and logistics for backup and bridging power. Cybersecurity for operational technology (which is a different discipline from IT security). Workforce. Ongoing operations and maintenance. Site security. Environmental compliance. Communications infrastructure.

Each of these is a category. Each category is hiring. And because the projects are moving faster than typical utility timelines, the supplier benches are forming right now. Not in 2030.

There’s a simple test for whether a market is still open. Ask whether the major buyers have settled on their preferred suppliers yet. For hyperscaler energy projects, the answer is likely, mostly no. Microsoft, Amazon, Meta, and Google are all building these supplier relationships in real time, right now. The companies that get in the door now are establishing track records that will matter for the next 20 years of buildout. OMSDC and NMSDC need to be at the forefront of helping to knock on those doors.

Because the companies that wait until the RFPs are published are likely to be competing for second-tier work after the primary benches are locked in.

Why This Is Happening Now

It’s worth understanding why this shift is occurring, because the explanation tells you whether this is a moment or a movement.

The short answer is that the utility model simply cannot deliver what the largest customers need on the timelines they require. Not anymore. Especially with our ageing infrastructure and lack of investment in that infrastructure.

A new transmission line in the United States takes 10 to 15 years to permit and build. Connecting a new data center to the grid in many markets takes three to seven years. The largest hyperscalers are planning capacity expansions on 18 to 36 month cycles, driven by AI training and inference demand that didn’t even exist five years ago. Waiting for the grid to catch up is not an option. The perceived economics of being late to AI are orders of magnitude larger than the cost of building your own power.

Add to that the carbon commitments these companies have made. Microsoft has pledged to be carbon negative by 2030. Google and Amazon have similar targets. Buying generic grid power, which still includes substantial fossil generation in most regions, doesn’t get them to those goals. Signing direct deals for nuclear, geothermal, or behind-the-meter renewable generation does. While the current Administration has been anti-Green, the carbon commitment is still a policy lever. The infrastructure deal is how these companies can execute on their commitment.

Finally, regulatory uncertainty is pushing in the same direction. With the current federal posture pulling back on parts of the clean energy agenda, hyperscalers cannot count on policy to deliver the energy mix they’ve committed to. So they’re building it themselves.

None of these forces are temporary. The economics of AI compute, the carbon commitments, and the regulatory volatility are all multi-decade phenomena. This is a movement, not a moment.

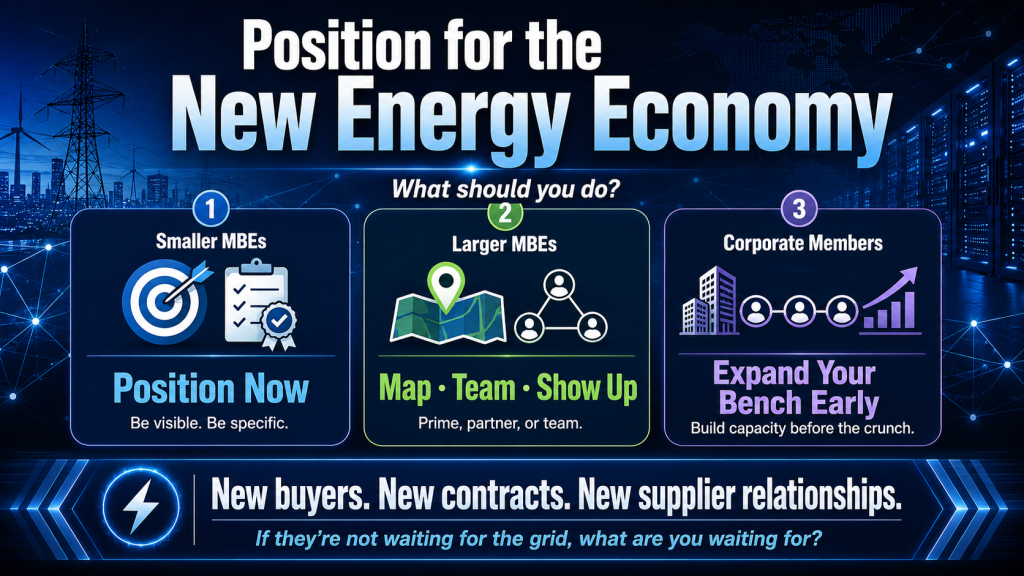

What Should You Do?

For smaller MBEs:

If your business touches any part of the energy buildout, even tangentially, this is the year to position. That includes electrical contracting, HVAC and mechanical work, civil construction, trucking and fuel logistics, security services, environmental consulting, IT and OT cybersecurity, facilities maintenance, and specialty trades. Get your certifications current. Get your capability statement specific to the energy and data center sector, even if most of your work has been in other industries.

The biggest mistake here would be assuming you need to be an “energy company” to participate. You don’t. The hyperscalers are buying the same services any large industrial project would need, from suppliers who can deliver on infrastructure timelines.

For larger MBEs:

Map your capabilities against the supplier categories above and identify where you can compete for primary work, where you can compete as a tier-two partner under a larger prime, and where teaming with another MBE would expand your range. The pursuit pod model from our recent Growth Under Pressure white paper applies directly here. A single MBE may not have the breadth to bid a full energy project. Three MBEs together often can.

Also begin the conversations with hyperscaler procurement teams now, before the formal RFP process opens. These companies are sourcing relationally as well as transactionally. The firms that are known, that have shown up, that have documented their capabilities and references in the right way, will be the firms that get called.

For corporate members:

If you operate in or around the energy, manufacturing, or technology sectors, your supplier base is about to be tested by buildout demand you may not have forecast. The same shortage of qualified labor and qualified suppliers that’s driving hyperscaler decisions is going to affect every adjacent industry. Now is the time to expand your supplier bench, not after the constraint becomes a crisis.

For procurement teams specifically: the suppliers who serve hyperscaler projects effectively will become the most sought-after firms in the country over the next decade. Being in those relationships early is a competitive advantage. Being in those relationships through OMSDC’s network is a way to find capable firms before they’re booked.

The Takeaway

For most of the last century, the question of who supplied energy was answered by who held the utility franchise. That question is being reopened. The largest customers in the country have decided they can no longer wait for the grid to deliver what they need, when they need it, in the form they need it.

That decision creates a new energy economy with new buyers, new contracts, and new supplier relationships forming in real time. The companies that recognize what’s happening will help build it. The companies that don’t will read about it in five years and wonder how they missed the opening.

Next month, we’ll cover the constraint that’s becoming a bigger problem than the power itself, and the supplier opportunity hiding inside it.

Until then, the question to sit with is simple. If the biggest energy customers in the country are no longer waiting for the grid, what are you waiting for?